Charitable Giving Facts

Support a worthy cause which may lower your tax bill

Charitable giving is a powerful financial tool. It provides double satisfaction — by helping a worthy cause, and possibly lowering your tax bill.

Perhaps you want to support your favorite charity or create a new program to address a specific concern in your community; whatever your personal goals, charitable giving can help you achieve them. In fact, charitable giving strategies often provide solutions unavailable through traditional estate planning.

Three valuable tax benefits

- You may receive an income tax deduction in the year you make the gift

- The federal gift tax does not apply to charitable gifts

- Charitable gifts may help reduce your potential estate tax liability

Other benefits

- Transform an illiquid asset into an important source of future income

- Restructure a non-diversified portfolio without incurring an immediate capital gain

- Help avoid current capital gains tax on the sale of a business

- Take an immediate tax deduction on a future gift

Easy charitable gifting

For an outright gift — in the form of money or property, to be income tax deductible, it must be for the charity’s benefit and the charity must take possession immediately.

Charitable giving vehicles

There are a number of tools and strategies that can be used for effective philanthropy, including:

- Qualified charitable distributions – Individuals over age 70½ can donate up to $100,000 from an IRA directly to a qualified charity without triggering any federal income taxes. A QCD distribution allow you to reduce taxable income, achieve charitable giving goals and satisfy your required minimum distribution — all in one transaction.

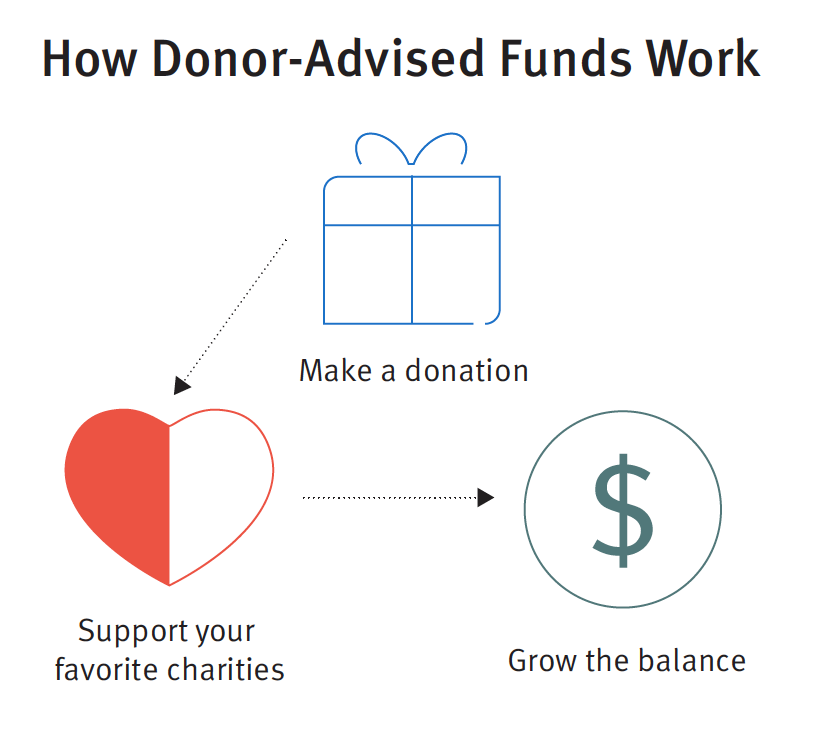

- Donor Advised Funds (DAF) — may be used by clients who intend to give to charities over time and who want to maximize their current income tax deductions. The benefits are similar to those of a private foundation, without all of the paperwork and start-up costs. Additional contributions can be made at any time with an additional tax deduction. Contributions are invested by the donor’s financial advisor.

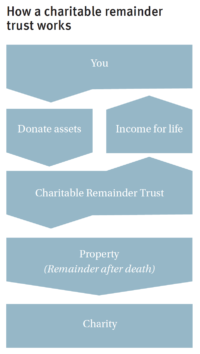

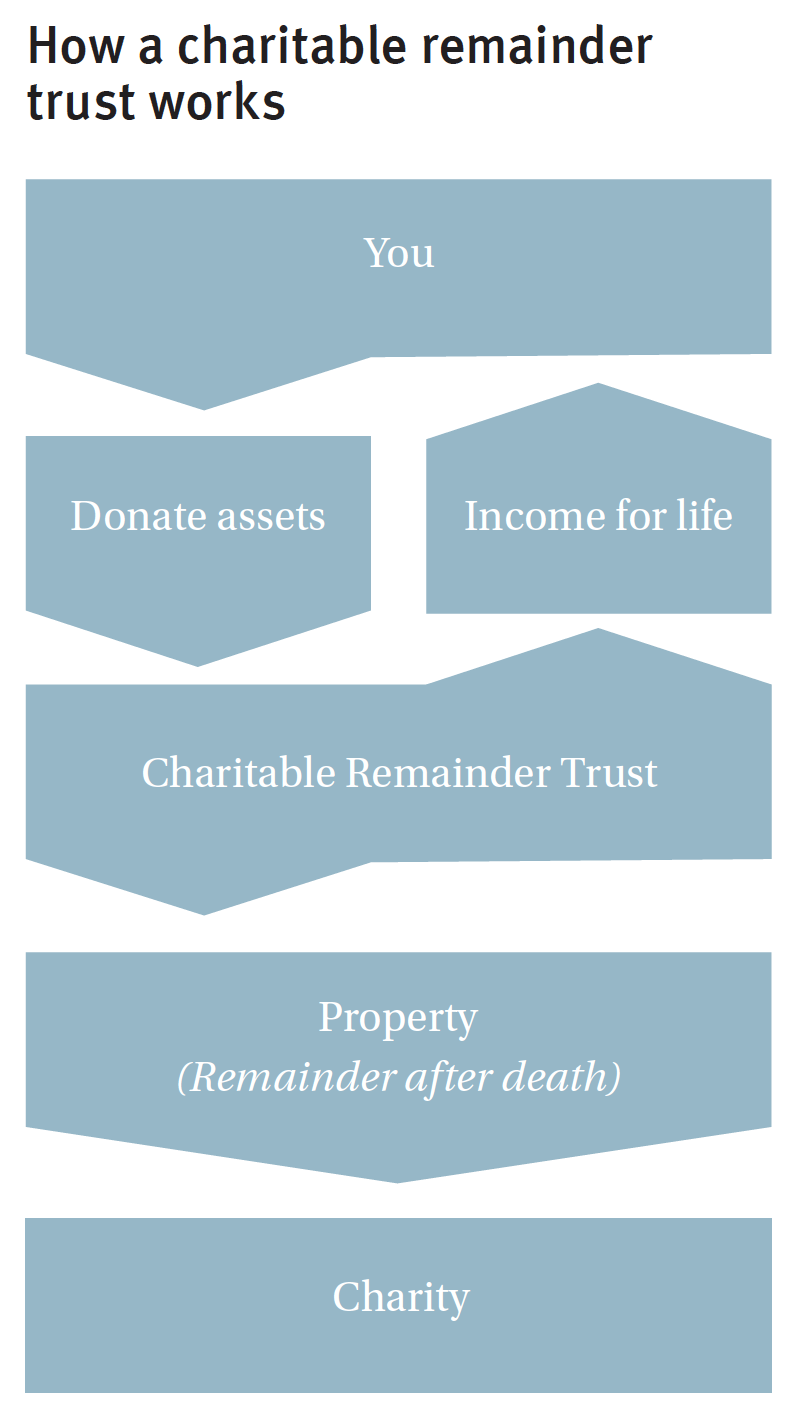

- Charitable Trusts — are irrevocable trusts established to receive gifts of cash or other property on behalf of a qualified charitable organization. Charitable Remainder Trust (CRT) allows the donor, and/or other family members, to receive a lifetime payment from the trust, or for a term not to exceed 20 years. Upon the death of the income beneficiaries, the trust is dissolved and the charity receives the remaining assets. Benefits of CRTs include the ability to help avoid capital gains tax on the sale of assets within the trust and a potential tax deduction when the trust is created.

- Charitable Remainder Annuity trust — A split interest trust that pays out a fixed amount of income every year (an annuity) based on the initial contribution to the trust to the non-charity beneficiary for the term of the trust, and the remaining assets pass to the charity at the end of the term.

- Charitable Remainder Unitrust — A split interest trust that pays the non-charity beneficiary a fluctuating amount each year, based on the value of the assets in the trust each year. At the end of the trust term, the remaining assets pass to the charity.

- The opposite of a CRT, a Charitable Lead Trust (CLT), provides an income to charity over a specified period (either the lifetime of one or more people, or over a set number of years). At the end of the period, the trust is dissolved and the remaining assets are distributed back to the donor or other named non-charitable beneficiaries. A CLT may enable the donor to transfer property to family members at a fraction of the fair market value.

- Private Foundations — enable a donor to establish their own private or family charitable organization to express the charitable wishes of the family in perpetuity. There are many options regarding the structure (trust or corporation) and management of a private foundation. Control over grants from the foundation and investments within the foundation remain with the donor and the family. Because of the complexity and costs, a private foundation is usually only established for considerable assets.

- Life insurance — enables a donor to make a significant lifetime gift to charity for a relatively small, tax-deductible annual contribution. Existing or new policies may be donated, subject to state law. Gifts of life insurance provide many benefits to the receiving charity, including minimal administration requirements, no delays in settlement, and the ability to access the policy cash values during the donor’s lifetime.

- Remainder interest in a residence — arrangements enable a donor to transfer title of property to a charity, while continuing to occupy and enjoy the property for either the life of the tenants or a specified period of time.

Start planning your giving strategy today

Working with an RBC Wealth Management financial advisor and using the RBC WealthPlan tool, you and your financial advisor can create a personal roadmap based on your vision for giving.

Your financial advisor has access to professional trustees and charitable entities that can assist in crafting your specific charitable giving plan and guide you through any complexities.

Contact your financial advisor today to discuss the benefits of charitable giving.

Trust services are provided by third parties. Neither RBC Wealth Management nor its financial advisors are able to serve as trustee. RBC Wealth Management does not provide tax or legal advice. All decisions regarding the tax or legal implications of your investments should be made in connection with your independent tax or legal advisor.